China’s Lehman Moment? Unpacking the Zhongrong Trust Crisis and Its Global Implications

A Comparative Analysis of the Zhongrong Trust Crisis and the Collapse of Lehman Brothers

Primary Sources: Investopedia and CNN

Introduction

In the fast-paced world of global finance, some events mark critical turning points. One such moment was the “Lehman Moment”—when the collapse of Lehman Brothers in 2008 triggered a worldwide financial crisis. Today, as China faces mounting debt, real estate turmoil, and weakening consumer confidence, many ask: Is the world’s second-largest economy nearing its own Lehman Moment—or drifting quietly into a deeper, more silent collapse?

Understanding these macroeconomic shifts isn’t just for economists—it’s vital for traders too. At FastPip, we help traders stay ahead of the curve through real-time market signals and copy trading strategies designed for global events like these. Whether you analyze markets yourself or prefer to follow expert traders, FastPip gives you the tools to react smartly when volatility strikes.

What Is a Lehman Moment?

A “Lehman Moment” refers to a sudden and severe turning point in the financial system, where the collapse of a major financial institution triggers a widespread loss of confidence, market panic, and systemic risk. The term originated from the fall of Lehman Brothers, the fourth-largest investment bank in the United States, which filed for bankruptcy on September 15, 2008. This event is widely regarded as the catalyst for the global financial crisis of 2008.

Core Characteristics of a Lehman Moment:

- Institutional Collapse with Systemic Reach

The downfall involves a major player whose financial obligations are deeply interconnected with other institutions, such that its failure sets off a domino effect. - Sudden Liquidity Freeze

Following the collapse, interbank lending and credit markets seize up. Banks and institutions no longer trust each other, causing liquidity to dry up overnight. - Investor Panic and Market Volatility

Confidence vanishes. Stock markets plunge, bond yields spike, and investors rush to sell off risk assets and flee to safe havens like gold or government bonds. - Global Spillover

Although the trigger may originate in one country, the contagion spreads rapidly across borders due to financial globalisation, impacting economies worldwide. - Policy Shock and Emergency Response

Governments and central banks scramble to respond with bailouts, interest rate cuts, and stimulus packages to prevent a complete financial meltdown.

The 2008 Example: Why Lehman Was Unique

Lehman Brothers’ collapse wasn’t merely about a single firm going under—it revealed deep vulnerabilities in the global financial system. The bank was highly leveraged, with exposure to toxic subprime mortgage assets. Once housing prices declined and mortgage defaults soared, the value of Lehman’s assets collapsed. But the broader danger was this:

- Lehman was counterparty to thousands of derivatives and lending contracts. Its failure left counterparties uncertain about their own risk exposures.

- Financial institutions hoarded cash, fearing who might be next to fail. This led to a freezing of credit markets.

- AIG, a global insurer, teetered on collapse within 48 hours, needing a U.S. government rescue due to its exposure to credit default swaps linked to Lehman.

- Money market funds broke the buck, sparking panic even among conservative investors.

The moment revealed that even a single failure in a tightly interwoven financial network can endanger the entire system.

Use of the Term Today

Since 2008, the phrase “Lehman Moment” has become a metaphor and warning signal. It is now commonly used by economists, policymakers, and financial media to describe:

- A systemic risk event waiting to happen

- A tipping point where trust collapses

- A moment when regulatory oversight has failed to detect a systemic buildup of risk

For instance, potential Lehman Moments have been speculated around:

- The European debt crisis (2010–2012)

- The Evergrande real estate collapse in China (2021)

- The Zhongrong Trust crisis (2023–2025), which this article explores in depth

Key Insight

A Lehman Moment is not just a corporate failure—it’s a psychological shift. It is the precise point when market optimism gives way to fear, when investors and institutions no longer believe in the solvency or stability of the system. Once trust evaporates, even solvent entities can fall victim to runs, fire sales, and forced deleveraging.

In essence, a Lehman Moment is the financial equivalent of an earthquake: the stress builds quietly over time, until one snap sends shockwaves through the system.

The 2008 Financial Crisis: Roots and Repercussions

The crisis stemmed from excessive risk-taking in the mortgage markets…

- Global GDP fell from 4.3% (2007) to -1.3% (2009)

- 30+ million jobs lost globally

- Emerging markets faced capital flight

Role of Credit Rating Agencies

Credit rating agencies—primarily Moody’s, Standard & Poor’s (S&P), and Fitch Ratings—played a central and controversial role in the global financial crisis of 2008. Their misclassification of risky financial products as safe investments contributed directly to the build-up of systemic risk, misinformed investors, and amplified the eventual collapse.

What Are Credit Rating Agencies?

Credit rating agencies (CRAs) are private companies that assess the creditworthiness of borrowers, ranging from corporations and countries to individual debt instruments like bonds and structured finance products. Their ratings (e.g., AAA, BBB, junk) help investors assess default risk and determine interest rates for loans.

Investors worldwide—pension funds, insurance companies, hedge funds—rely on these ratings to guide portfolio decisions. In theory, high-rated products are low risk and safe for capital preservation.

How They Failed: The Structured Finance Trap

In the early 2000s, CRAs began rating mortgage-backed securities (MBS) and collateralized debt obligations (CDOs), complex financial instruments composed of bundled subprime mortgages. Despite the questionable quality of the underlying loans, many of these securities received top-tier AAA ratings.

Here’s how the distortion happened:

- Lack of transparency: CRAs often didn’t fully understand the complexity of the products they were rating, or the risks embedded in them.

- Issuer-pays model: Banks and financial institutions that created these products also paid the CRAs to rate them. This created a conflict of interest, as agencies had a financial incentive to assign favourable ratings to secure more business.

- Modelling flaws: Rating agencies used outdated risk models that underestimated the likelihood of widespread mortgage defaults, especially in a nationwide housing downturn.

- Competitive pressure: The “Big Three” CRAs competed fiercely for market share. If one agency was too conservative, banks would shop around for a more favourable rating—a practice known as “ratings shopping.”

Consequences of Inflated Ratings

- False sense of security: AAA ratings on subprime-backed securities misled investors into believing these were safe investments.

- Massive exposure: Pension funds, university endowments, and foreign banks loaded up on these “safe” products, unaware of the true risk.

- Delayed reactions: As defaults rose, CRAs were slow to downgrade these securities. When they eventually did, the downgrades came all at once—triggering fire sales, liquidity crises, and catastrophic losses.

- Global contagion: Because these products were sold worldwide, the damage wasn’t contained to U.S. banks. European institutions (e.g., Dexia, UBS) suffered billions in losses from AAA-rated toxic assets.

Investigations and Backlash

In the aftermath of the crisis, rating agencies faced intense scrutiny:

- The U.S. Senate Permanent Subcommittee on Investigations held hearings, revealing internal emails that showed rating analysts were aware of the risks but continued assigning high ratings.

- One infamous email from an S&P employee read: “Let’s hope we are all wealthy and retired by the time this house of cards falters.”

- Lawsuits were filed by investors, states, and the U.S. Department of Justice against all three major CRAs for negligence and misrepresentation.

- The Dodd-Frank Wall Street Reform and Consumer Protection Act (2010) imposed stricter oversight on CRAs, including:

- Increased transparency in rating methodologies

- Legal liability for misleading ratings

- Mandatory disclosure of conflicts of interest

- Creation of the Office of Credit Ratings within the SEC

Long-Term Implications

The crisis permanently damaged the credibility of credit rating agencies. While their services remain integral to global finance, investors, regulators, and financial institutions have grown more sceptical and now often supplement ratings with independent risk analysis.

Today, references to “AAA-rated” securities are no longer taken at face value. The 2008 crash reminded the world that a high rating does not equal low risk, especially when profit motives compromise objectivity.

Lehman Brothers’ Collapse in Focus

Lehman Brothers, founded in 1850, was one of the most prominent and prestigious investment banks on Wall Street. By the early 2000s, it had grown into a global financial powerhouse with operations in equities, fixed income, investment banking, and, crucially, real estate finance.

But behind its success story was a dangerous overreliance on leverage, excessive exposure to the housing market, and a lack of transparency—factors that ultimately led to one of the largest bankruptcies in U.S. history.

Aggressive Expansion into Subprime Lending

In the early 2000s, Lehman aggressively pursued profits in the booming real estate market. The firm:

- Acquired subprime lenders such as BNC Mortgage and Aurora Loan Services

- Packaged risky mortgages into mortgage-backed securities (MBS) and sold them to investors globally

- Borrowed heavily to fund its positions, often maintaining a leverage ratio of more than 30 to 1, meaning for every $1 in equity, it had borrowed $30

While this strategy was profitable during the housing boom, it made Lehman highly vulnerable to even a modest downturn in property prices.

Cracks Begin to Show

By 2007, early signs of stress emerged:

- Rising mortgage delinquencies and defaults undermined the value of Lehman’s mortgage-backed assets

- In Q2 2008, Lehman reported a $2.8 billion loss—its first quarterly loss since going public in 1994

- The firm attempted to reassure investors through restructuring and selling parts of its business, but confidence continued to erode

Efforts to raise capital through sovereign wealth funds and private investors failed. Ratings agencies downgraded Lehman’s credit, increasing its borrowing costs and deepening the liquidity crisis.

The Final Days

In the week leading up to September 15, 2008, Lehman desperately sought a buyer:

- Talks with Barclays and Bank of America collapsed when U.S. regulators refused to provide guarantees for Lehman’s toxic assets

- Unlike the Bear Stearns rescue months earlier, the U.S. government declined to bail out Lehman, citing concerns over “moral hazard”

On September 15, 2008, Lehman Brothers filed for Chapter 11 bankruptcy protection, listing $639 billion in assets and $619 billion in debt, making it the largest bankruptcy in U.S. history at the time.

Immediate Aftershocks

The collapse triggered a wave of financial chaos:

- The S&P 500 dropped 5% in a single day, and global stock markets tumbled

- The money market fund “Reserve Primary Fund” broke the buck, sparking fears even in the safest investment vehicles

- Financial institutions worldwide began hoarding cash, freezing interbank lending markets

- Within 48 hours, AIG faced collapse due to exposure to Lehman-linked derivatives, requiring a $182 billion government bailout

- Investment bank Merrill Lynch was forced into a shotgun merger with Bank of America

- Global credit markets froze, making it nearly impossible for companies to borrow or refinance

Long-Term Implications

The Lehman bankruptcy:

- Destroyed over $10 trillion in global equity markets within weeks

- Forced unprecedented interventions by central banks worldwide, including quantitative easing and near-zero interest rates

- Exposed the fragile underpinnings of the shadow banking system

- Sparked a reevaluation of risk models, regulatory frameworks, and crisis preparedness

It also galvanized political responses, including:

- The Troubled Asset Relief Program (TARP): A $700 billion bailout fund for U.S. financial institutions

- The Dodd-Frank Act (2010): Comprehensive financial reform to limit systemic risk and improve oversight

Why Lehman Was Allowed to Fail

One of the most debated questions in modern financial history is: Why did the U.S. let Lehman fail, but not Bear Stearns or AIG?

Key reasons include:

- Lack of willing buyers and too little time to arrange a deal

- Political pressure not to use taxpayer funds again after Bear Stearns

- The belief that markets could absorb the shock

That decision, however, proved to be a miscalculation, as the fallout was far worse than anticipated and forced even larger bailouts afterwards.

Legacy

Lehman Brothers became a symbol—not just of corporate failure, but of systemic fragility, flawed oversight, and the global consequences of interconnected finance. Its collapse remains a case study in:

- The dangers of overleveraging

- The perils of unchecked financial innovation

- The need for crisis planning and transparency in financial institutions

It is the quintessential Lehman Moment—the point where trust vanished, panic spread, and the world economy shifted into crisis mode.

China’s Shadow Banking and Zhongrong Trust

What Is Shadow Banking?

“Shadow banking” refers to non-bank financial institutions and intermediaries that engage in credit creation and lending activities outside the formal banking system. These entities do not take deposits like traditional banks and are often less regulated, making them more opaque and risk-prone.

In China, the shadow banking sector includes:

– Trust companies

– Wealth management products (WMPs)

– Asset management firms

– Entrusted loans

– Local government financing vehicles (LGFVs)

The sector expanded rapidly after the 2008 financial crisis, as policymakers encouraged alternative financing channels to support China’s high-growth model. By some estimates, shadow banking in China peaked at over 80% of GDP in the late 2010s.

While shadow banks provided critical liquidity to private firms, real estate developers, and local governments, they also increased systemic risk by:

- Operating with weak oversight

- Engaging in maturity mismatches

- Financing speculative and high-risk projects

- Creating complex, interlinked obligations with unclear ultimate risk holders

Introducing Zhongrong Trust

Zhongrong International Trust Co., founded in 1987 and headquartered in Beijing, was one of China’s largest and most active trust companies.

- As of early 2023, Zhongrong managed over $87 billion in assets

- It was part of the broader Zhongzhi Enterprise Group (ZEG), a financial conglomerate overseeing over 1.13 trillion yuan (~$138 billion) in total assets

- Zhongrong was deeply involved in high-yield trust products, many of which channelled funds into real estate, infrastructure, and private equity

These trust products were popular among wealthy individuals, corporations, and state-owned enterprises seeking returns higher than bank deposits. However, many investors mistakenly believed these products were implicitly backed by the state—a perception that would later prove dangerously wrong.

The 2023 Crisis: Zhongrong Defaults

In mid-2023, reports emerged that Zhongrong Trust had failed to make payments to several corporate clients and product holders. Companies like:

- Nacity Property Services

- KBC Corporation

- Xianheng Technology

publicly disclosed that Zhongrong missed maturity payments worth millions of yuan. The defaults were not isolated—multiple similar cases followed, revealing widespread illiquidity within the firm.

Soon after:

- Protests erupted outside Zhongrong’s Beijing office, as retail and institutional investors demanded repayment

- Leaked internal memos and whistleblower reports suggested cash shortfalls, management disarray, and misuse of client funds

Why Did Zhongrong Fail?

- Overexposure to Real Estate

More than 10% of Zhongrong’s investment portfolio was tied to China’s struggling real estate sector—an industry facing severe headwinds from regulatory crackdowns and falling housing demand. - Liquidity Mismatch

Zhongrong promised high short-term returns, but invested in long-term, illiquid projects. As redemptions rose, cash dried up. - ZEG’s Internal Crisis

Zhongzhi Enterprise Group, the parent company, faced its financial strain. Other subsidiaries reportedly missed payroll, paused operations, and sought restructuring. - Lack of State Bailout

Unlike previous instances where local governments or SOEs stepped in, authorities chose not to bail out Zhongrong, signalling a shift in China’s approach to “moral hazard.”

Broader Implications for Shadow Banking

Zhongrong’s collapse was not an isolated event—it was symptomatic of deep structural issues in China’s financial system:

- Loss of trust in wealth management products

- Heightened investor risk awareness

- Fears of contagion to other trust firms like Zhongtai Trust and CITIC Trust

- Speculation about financial instability spreading to local government platforms and commercial banks with indirect exposure

By 2024, regulators imposed stricter rules on trust companies, increased disclosure requirements, and expanded the scope of financial inspections. However, tens of billions of yuan remained frozen, and full repayment to investors remained uncertain.

Summary

Zhongrong Trust’s crisis revealed the fragile foundation of China’s shadow banking system: rapid, debt-fueled growth built on opaque products and unrealistic investor expectations. Unlike the spectacular crash of Lehman Brothers, Zhongrong’s downfall was quieter, but just as dangerous, undermining faith in alternative finance, weakening consumer sentiment, and exposing the limits of regulatory control in a hybrid financial economy.

Its story is now seen as a turning point in Beijing’s long-running struggle to reform shadow banking without destabilising the broader financial system.

Comparing Lehman and Zhongrong

| Metric | Lehman Brothers (U.S.) | Zhongrong Trust (China) |

|---|---|---|

| Type of Institution | Investment Bank | Trust / Wealth Mgmt |

| Core Trigger | Subprime Collapse | Real Estate Slump |

| Gov’t Response | Bailouts | Silent Containment |

| Impact | Global | Domestic |

| Style | Explosive | Gradual |

Public and Media Reaction

🇺🇸 United States: Transparency and Outrage

The collapse of Lehman Brothers in 2008 triggered a wave of public anger across the U.S. Political leaders faced immense pressure to explain how Wall Street was allowed to take such reckless risks. Key reactions included:

- Nonstop media coverage: Major networks and newspapers ran daily investigations into the causes of the crisis.

- Congressional hearings: Executives from Lehman, AIG, and major banks were summoned before Congress.

- Public protests: Movements like Occupy Wall Street later emerged, fueled by anger over bailouts and income inequality.

- Regulatory reform debates: The media played a central role in shaping support for reforms like the Dodd-Frank Act.

The U.S. response was marked by transparency, public accountability, and political mobilisation, even if the outcomes remained controversial.

🇨🇳 China: Control and Containment

In contrast, when Zhongrong Trust’s defaults came to light in 2023, the Chinese government moved quickly to suppress panic and control the narrative:

- Censorship of news coverage on platforms like WeChat, Weibo, and state-run media

- Blocking of protest footage and keywords, including “trust crisis” and “Zhongzhi default”

- Media silence on broader shadow banking risks to avoid fueling public concern

- Targeted detentions and warnings for protesters and whistleblowers

Rather than transparency, China’s strategy prioritized stability and silence. While effective in avoiding immediate panic, it left many investors confused and distrustful.

Market Reaction and Expert Opinions

Market Reaction

Market Reaction

The news of Zhongrong Trust’s missed payments in 2023 sent ripples through China’s financial markets:

-

Real estate and financial stocks in Shanghai and Hong Kong experienced sharp declines.

-

The Chinese yuan weakened briefly, reflecting investor uncertainty.

-

Investor forums and social media were flooded with speculation about which companies might be exposed.

-

Some publicly listed firms were pressured to disclose counterparty risk to Zhongrong-linked products.

Despite the controlled media environment, market signals pointed to growing unease about shadow banking stability.

Expert Analysis

Nomura’s View

Nomura analysts raised strong concerns, describing Zhongrong’s troubles as a sign of systemic fragility within China’s financial ecosystem. Their research highlighted:

-

Deep exposure of Zhongzhi Group to distressed property developers

-

Risk of spillover into household consumption, as many retail investors had trust product exposure

-

Possible drag on China’s GDP growth if trust sector contagion spreads

They warned that if defaults continued, investor confidence could collapse across the broader wealth management sector.

Citi’s View

Citi took a more measured stance, arguing that while the situation was serious, it did not constitute a Lehman-style collapse. Their key points included:

-

Most trust products were closed-ended, limiting the risk of immediate redemption runs

-

Since 2017, regulators have reduced banks’ off-balance-sheet exposure

-

As of early 2025, real estate-linked trust products made up just 0.3% of total financial system assets

Citi concluded that the crisis was contained and reflected structural adjustments, not systemic failure.

China in 2025: Crisis Over or Delayed?

Two years after the Zhongrong Trust defaults, the question remains: has China truly stabilized, or is it merely postponing a deeper financial reckoning? While no Lehman-style shock has occurred, structural vulnerabilities persist and suggest the crisis may be delayed, not avoided.

🔻 Foreign Direct Investment (FDI) and Capital Outflows

-

Global firms have increasingly relocated supply chains to Southeast Asia, India, and Mexico due to rising geopolitical tensions.

-

FDI inflows into China declined for a third consecutive year in 2025, reflecting concerns over regulatory opacity and political risk.

-

Capital outflows—especially by high-net-worth individuals—have pressured the yuan and limited domestic reinvestment.

Weakened SMEs and Labour Market Strain

-

Small and medium-sized enterprises (SMEs), long considered the backbone of China’s private economy, face shrinking credit access and sluggish demand.

-

Widespread cost-cutting and hiring freezes have contributed to rising urban youth unemployment and stagnant wage growth.

Continued Mistrust in Trust Products

-

Following the Zhongrong defaults, many investors remain wary of non-bank financial products.

-

Demand has shifted toward state-backed instruments and foreign asset diversification, further draining liquidity from the private sector.

Persistent Real Estate Overhang

-

Major developers like Evergrande and Sunac remain in restructuring.

-

Housing prices in Tier-2 and Tier-3 cities continue to decline or stagnate, eroding household wealth.

-

Local governments, which rely heavily on land sales, face fiscal shortfalls and rising debt burdens.

➤ Verdict

While surface indicators may suggest stability, the underlying fundamentals reveal a sluggish, risk-averse, and structurally constrained economy. Rather than a dramatic collapse, China appears to be navigating a long, slow unwinding—a silent financial squeeze that could define the next phase of its economic evolution.

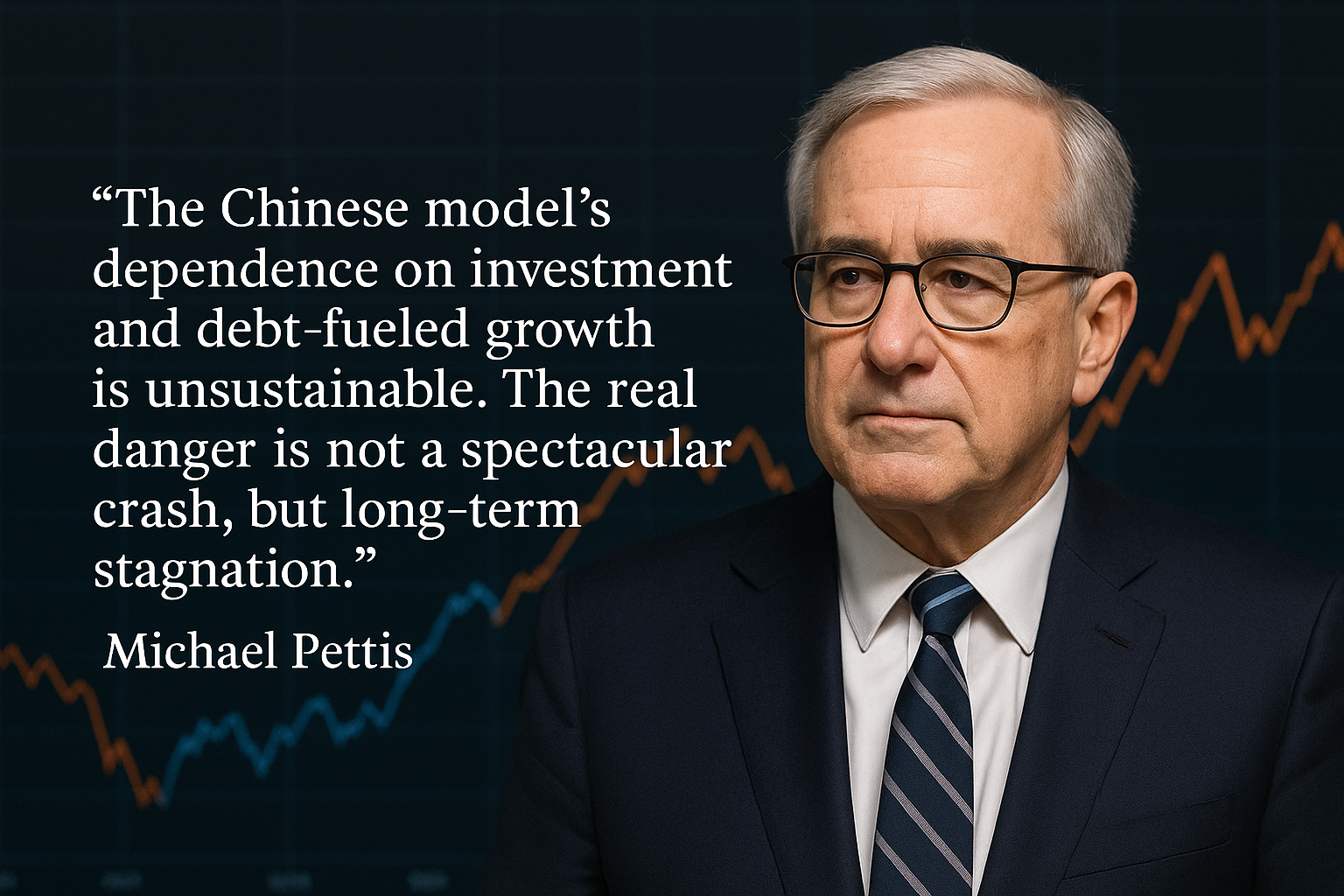

Michael Pettis’ Analysis

“The Chinese model’s dependence on investment and debt-fueled growth is unsustainable. The real danger is not a spectacular crash, but long-term stagnation.”

Final Verdict: China’s Silent Lehman Moment

While China has thus far avoided a dramatic, headline-grabbing collapse like Lehman Brothers in 2008, the Zhongrong Trust crisis has exposed deep structural weaknesses in the heart of the Chinese financial system. Rather than a single, catastrophic event, China appears to be undergoing a slow-motion financial unwinding—one that is less visible, but potentially just as consequential.

A Crisis Without Shockwaves

Unlike the Lehman bankruptcy, which triggered global panic in a matter of days, Zhongrong’s crisis unfolded gradually and was largely contained within China’s borders. However, this containment came at a cost:

-

Investor trust eroded silently, without official acknowledgement.

-

Shadow banking shrank, cutting off credit to vital sectors like SMEs and real estate.

-

Household risk appetite diminished, fueling savings hoarding and consumption fatigue.

The result is a form of financial stagnation that does not make front-page news, but slowly saps the vitality of private sector growth and innovation.

Systemic Issues Still Unresolved

The government’s strategy—tight censorship, selective bailouts, and gradual regulatory tightening—has prevented widespread panic, but has not addressed the root causes:

-

Excessive leverage in real estate and local government platforms

-

Lack of transparency in financial products

-

Weak consumer sentiment and confidence

-

Overreliance on state-led investment for GDP growth

China’s dual-track financial system—where state-owned institutions remain protected and private players face tightening constraints has led to increasing market bifurcation and capital misallocation.

The Silent Lehman Moment

This unfolding crisis could be termed a “Silent Lehman Moment”—not because of what it explodes, but because of what it corrodes:

-

Trust

-

Risk-taking

-

Private sector momentum

As Michael Pettis and other economists argue, the real threat is not collapse, but long-term stagnation masked by stability on the surface. It is a crisis that plays out not in panic, but in reduced dynamism, credit contraction, and eroded confidence.

Conclusion

China’s financial system in 2025 stands at a crossroads. The immediate danger may have passed, but without bold structural reform, the country risks drifting into a prolonged phase of low-growth fragility, a quiet crisis that reshapes the future of Chinese finance and its global role.

In the end, the question is no longer whether China will face a Lehman Moment. The question is whether it is already living through one, in silence.

Sources

- Investopedia – What Is a Lehman Moment?

- CNN Business – China’s ‘Lehman moment?

- World Bank GDP Reports (2007–2010)

- Michael Pettis Interview – Foreign Policy, 2024

- Reuters – China shadow bank crisis sparks calls for policy response

- Top 10 World Economies in 2025