Dynamic Money Management vs Fixed Money Management in Trading: The Professional Choice

Introduction

In trading, strategy attracts attention — but money management determines survival.

Many traders obsess over entry precision while underestimating position sizing, risk exposure, and capital allocation. Yet history consistently shows that accounts rarely fail because of one bad trade. They fail because of unstable risk management.

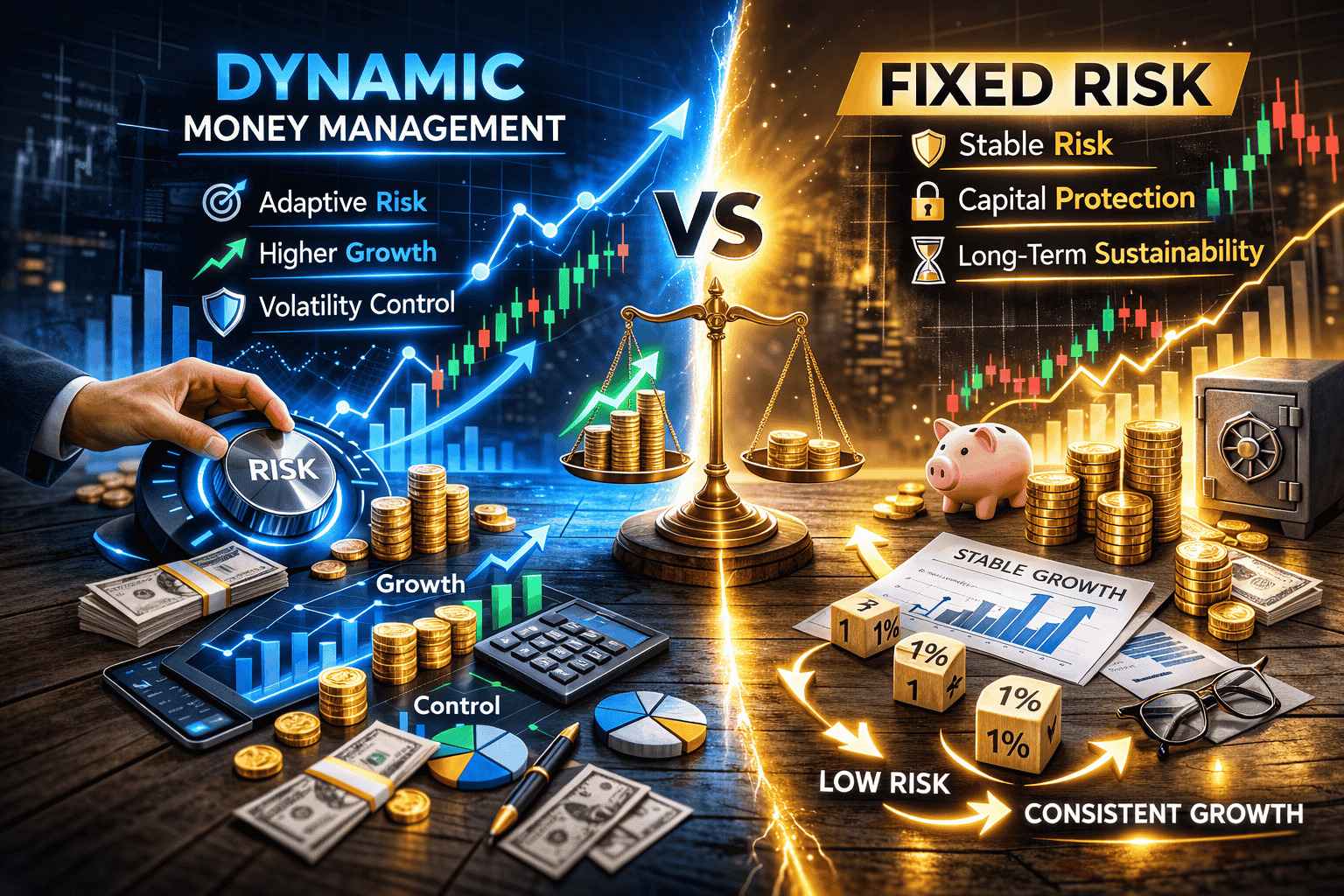

The debate between Dynamic Money Management and Fixed Money Management is not merely technical. It reflects two different philosophies of risk, growth, and long-term sustainability. Should risk remain constant regardless of circumstances? Or should it adapt to equity performance and market volatility?

This article provides a deep professional analysis of both approaches, examining their impact on growth, drawdown control, psychological stability, volatility exposure, and long-term capital compounding.

The goal is not to declare one universally superior — but to determine which approach is more professional under different trading conditions.

1. Why Money Management Is More Important Than Strategy

Most traders begin their journey by searching for a profitable system. They test indicators, explore price action patterns, study macroeconomic drivers, and refine entry timing. However, professional trading is not primarily about entries. It is about exposure.

If two traders use the same strategy but apply different risk allocation models, their long-term results can diverge dramatically. One may experience steady growth with manageable drawdowns. The other may face severe equity swings or even account destruction.

The mathematical reality is simple:

A profitable strategy without disciplined risk control can still lead to ruin.

Money management governs:

-

Position size

-

Maximum capital exposure

-

Drawdown tolerance

-

Compounding structure

-

Survival probability

Professional traders understand that the first objective in markets is not profit. It is survival. Without survival, compounding cannot occur.

This is where the distinction between Fixed Money Management and Dynamic Money Management becomes critical.

2. Understanding Fixed Money Management

Fixed Money Management is a risk allocation model in which a trader risks a constant percentage of account equity per trade.

This percentage remains stable regardless of recent wins, losses, volatility shifts, or emotional state.

For example:

-

Account balance: $20,000

-

Risk per trade: 1%

-

Maximum loss per trade: $200

If the account grows to $30,000, 1% becomes $300.

If it declines to $15,000, 1% becomes $150.

The percentage remains constant — the dollar amount adjusts automatically.

Core Characteristics

-

Predictable risk exposure

-

Stable variance profile

-

Minimal emotional decision-making

-

Automatic equity-based adjustment

This structure creates mathematical consistency. The equity curve may fluctuate, but risk exposure does not accelerate or decelerate unpredictably.

Benefits

-

Lower probability of catastrophic loss

-

Easier performance modeling

-

Psychological stability

-

Clean compounding structure

For traders building discipline, this simplicity is powerful.

However, fixed risk does not adapt to:

-

Volatility spikes

-

Structural market shifts

-

Strategy performance cycles

This limitation introduces the argument for dynamic models.

3. Understanding Dynamic Money Management

Dynamic Money Management adjusts position size based on predefined performance or market variables.

Risk may increase during strong performance phases and decrease during drawdowns.

Risk may also adapt to:

-

Volatility expansion

-

Portfolio correlation

-

Market regime changes

-

Statistical thresholds

In simple terms:

Fixed Model → Risk constant

Dynamic Model → Risk responsive

Dynamic models can be structured in multiple ways:

-

Performance-based scaling

-

Volatility-based scaling

-

Drawdown-based reduction

-

Kelly Criterion adjustments

-

Risk parity allocation

At an institutional level, dynamic risk allocation is common. Hedge funds rarely maintain completely static exposure across all environments.

However, the distinction between professional dynamic risk management and emotional risk adjustment is crucial.

Without strict rules, dynamic risk becomes:

Overconfidence during winning streaks

Fear-driven contraction during losses

Therefore, structure determines professionalism.

4. The Mathematics of Growth and Compounding

Compounding is the engine of long-term trading success.

With fixed risk, compounding is steady and proportional. Equity growth accelerates naturally over time without abrupt jumps in exposure.

With dynamic risk, compounding can accelerate faster during positive phases. However, the variance of returns increases.

Higher variance means:

-

Larger potential growth

-

Larger potential drawdowns

-

Greater equity instability

Professionals prioritize risk-adjusted return, not raw return.

A system generating 30% annual return with 10% drawdown may be more professional than one generating 50% return with 40% drawdown.

Fixed models tend to reduce variance.

Dynamic models can amplify it.

5. Drawdown Control and Survival Probability

Drawdown defines long-term survivability.

A 10% drawdown requires approximately 11% recovery.

A 30% drawdown requires 43% recovery.

A 50% drawdown requires 100% recovery.

Depth increases recovery difficulty exponentially.

Fixed risk creates predictable drawdown structures.

Dynamic risk can either mitigate drawdowns (if reduced appropriately) or intensify them (if increased at wrong time).

The core question is:

Does the trader have a statistically valid trigger for adjusting risk?

If not, fixed risk may offer superior survival probability.

Research published by the Federal Reserve consistently highlights the systemic dangers of excessive leverage and concentrated risk exposure.

6. Psychological Stability and Behavioral Risk

Markets test emotional resilience more than analytical skill.

Fixed risk reduces emotional volatility because exposure remains constant. There are no mid-cycle decisions about increasing or decreasing risk.

Dynamic risk introduces additional decision layers:

-

When to increase?

-

When to reduce?

-

By how much?

Each additional decision increases cognitive load and behavioral risk.

Many accounts fail not because of strategy failure, but because traders adjust exposure impulsively.

Professionalism requires rule-based structure, not reactive behavior.

7. Volatility Regimes and Risk Adaptation

Markets shift between:

-

Low volatility regimes

-

High volatility regimes

-

Trending environments

-

Range-bound phases

Fixed risk does not directly respond to volatility changes.

Dynamic risk can adapt using:

-

ATR-based sizing

-

Volatility index filters

-

Portfolio exposure adjustments

When executed quantitatively, this can enhance risk efficiency.

However, miscalibrated volatility adaptation can lead to overexposure during transition phases.

Volatility-adjusted position sizing concepts are commonly referenced in derivatives risk materials published by CME Group.

8. Institutional Practices and Professional Capital Allocation

Institutional investors rarely rely on purely fixed exposure.

They implement:

-

Value-at-Risk models

-

Maximum drawdown thresholds

-

Correlation-adjusted exposure

-

Volatility targeting

These are structured forms of Dynamic Money Management.

However, key difference:

Institutions operate with models, data infrastructure, and risk committees.

Retail traders often lack these layers.

Therefore, replicating institutional dynamic models without institutional structure can increase risk.

Structured risk governance frameworks used in professional portfolio management are widely discussed by the CFA Institute.

9. When Fixed Money Management Is More Professional

Fixed risk is often superior when:

-

Strategy data is limited

-

Trader discipline is still developing

-

Psychological tolerance for volatility is low

-

Account size is modest

-

Long-term consistency is priority

Professionalism is not complexity. It is consistency.

10. When Dynamic Money Management Creates Advantage

Dynamic risk can create competitive advantage when:

-

Strategy performance cycles are statistically validated

-

Volatility shifts are quantifiable

-

Drawdown thresholds are predefined

-

Risk caps are enforced

-

Execution is systematic

Without structure, dynamic becomes dangerous.

📊 Dynamic vs Fixed Money Management Comparison

| Criteria | Dynamic Money Management | Fixed Money Management |

|---|---|---|

| Risk Percentage | Variable | Constant |

| Adaptation to Volatility | High (if structured) | None |

| Drawdown Control | Potentially adaptive | Predictable |

| Growth Acceleration | Faster in strong phases | Steady |

| Variance of Returns | Higher | Lower |

| Psychological Pressure | Higher | Lower |

| Complexity | Advanced | Simple |

| Suitable For | Experienced / Quant traders | Most individual traders |

| Risk of Emotional Misuse | High | Low |

| Long-Term Stability | Depends on structure | Generally stable |

Conclusion: Which Is More Professional — Dynamic or Fixed Money Management?

After a comprehensive examination of growth mechanics, drawdown behavior, volatility adaptation, psychological stability, and long-term capital sustainability, we return to the central question:

Is Dynamic Money Management more professional than Fixed Money Management?

The precise answer is this:

Professionalism is not determined by whether risk is dynamic or fixed.

It is determined by whether risk is controlled, structured, and consistently executed.

However, when we evaluate both models through the lens of survival probability, behavioral stability, and long-term compounding efficiency, clear distinctions emerge.

Fixed Money Management: The Foundation of Professional Stability

Fixed Money Management provides:

-

Predictable exposure

-

Controlled variance

-

Lower probability of catastrophic drawdown

-

Simpler execution

-

Strong psychological stability

It minimizes behavioral errors because it removes discretionary exposure adjustments. There are no mid-cycle decisions about increasing risk after a winning streak or cutting exposure impulsively after losses.

For the majority of individual traders, this structural simplicity is not a limitation — it is an advantage.

In long-term trading careers, survival outweighs acceleration. Fixed risk models protect the compounding engine from disruption caused by emotional or mistimed exposure shifts.

If professionalism is defined as discipline, predictability, and controlled downside risk, Fixed Money Management represents the most reliable baseline.

Dynamic Money Management: Professional — But Only Under Strict Conditions

Dynamic Money Management can be more efficient — but only when executed within a rigorous quantitative framework.

It becomes professional when:

-

Risk adjustments are rule-based and predefined

-

Statistical thresholds trigger exposure changes

-

Maximum risk caps are enforced

-

Drawdown-based reductions are automatic

-

Volatility filters are data-driven

-

Execution is systematic, not emotional

When properly structured, dynamic risk models can:

-

Improve capital efficiency

-

Adapt to volatility regimes

-

Reduce exposure during structural weakness

-

Accelerate growth during statistically favorable phases

This is why hedge funds, quantitative desks, and institutional allocators use adaptive risk frameworks.

But here lies the critical distinction:

Institutions operate with deep data sets, risk oversight, and strict exposure controls.

Retail traders often attempt dynamic adjustments without this infrastructure — and that is where instability emerges.

Without statistical rigor, dynamic money management easily turns into:

-

Overconfidence after wins

-

Fear-based contraction after losses

-

Volatility amplification

-

Equity curve instability

In such cases, dynamic risk becomes a performance destabilizer rather than a professional edge.

The Real Professional Standard: Risk Governance

The debate between dynamic and fixed models ultimately reveals a deeper truth:

Professional trading is not about maximizing returns.

It is about governing risk.

Risk governance includes:

-

Defined maximum loss per trade

-

Defined maximum portfolio exposure

-

Defined maximum acceptable drawdown

-

Clear recovery protocols

-

Consistent execution rules

Whether the risk percentage is static or adaptive matters less than whether it is governed.

Uncontrolled fixed risk is dangerous.

Uncontrolled dynamic risk is catastrophic.

Governed risk — in either form — is professional.

Compounding and Longevity: The Decisive Factor

Markets reward longevity.

The power of compounding does not depend on explosive growth; it depends on uninterrupted participation. Deep drawdowns break compounding. Behavioral instability breaks execution. Exposure mismanagement breaks accounts.

Fixed models generally create smoother compounding curves.

Dynamic models may create steeper but more volatile curves.

Over a multi-year horizon, smoother compounding often outperforms aggressive acceleration interrupted by severe equity shocks.

The trader who survives five years consistently will likely outperform the trader who attempts to double the account in one year and resets repeatedly.

Which Model Is More Professional?

The structured answer:

-

For developing traders → Fixed Money Management is more professional.

-

For experienced traders with deep statistical validation → A controlled dynamic or hybrid model may be more efficient.

-

For institutional environments → Systematic dynamic allocation is standard, but within strict governance frameworks.

Professionalism is not complexity.

Professionalism is repeatability.

If a trader cannot execute a dynamic model without emotional interference, the model is not professional — regardless of theoretical sophistication.

The Final Principle

The most professional money management model is the one that:

-

Maximizes survival probability

-

Minimizes catastrophic risk

-

Supports stable compounding

-

Aligns with psychological tolerance

-

Can be executed consistently in adverse conditions

In trading, the objective is not to win aggressively.

It is to remain solvent long enough for statistical edge to manifest.

Markets do not reward excitement.

They reward discipline.

And discipline, above all else, defines professional money management.